For years, the narrative was simple: private cryptocurrencies like Bitcoin is a decentralized digital currency that operates without a central authority were the rebels, and governments were the slow-moving giants trying to catch up. But as we hit late 2026, that story has flipped. Governments aren't just watching anymore; they are building their own rivals. Central Bank Digital Currencies (CBDCs) have moved from theoretical whitepapers to active pilots in nearly every major economy on Earth.

This isn't just about updating payment systems. It’s a strategic move to reclaim control over money in a digital age. With 134 countries representing 98% of global GDP actively developing or exploring CBDCs, the landscape is shifting under our feet. The question is no longer if CBDCs will launch, but how they will compete with-and potentially restrict-the private crypto ecosystem you might already be using.

The Scale of the Shift: From Niche Experiment to National Priority

Let’s look at the numbers because they tell a stark story. In 2023, 114 countries were dabbling in digital currency ideas. By 2025, that number jumped to 134. This isn’t a niche tech experiment anymore; it is a global infrastructure project. Among these nations, 81 central banks are in the exploration phase, while 69 have moved into serious pilot and development stages.

Why does this matter to you? Because when the G20 nations commit resources, the rules change. Nineteen G20 countries are exploring CBDCs, and 16 are already in development or pilot phases. This includes economic powerhouses that set the tone for global finance. When the Reserve Bank of India expands its retail and wholesale CBDCs with offline functionality, or when the Bank of Japan runs methodical pilots focusing on user experience since April 2023, they are signaling that state-backed digital money is here to stay.

The actual deployment is still limited-only a handful of countries like the Bahamas, Nigeria, Jamaica, and Zimbabwe have fully launched-but the momentum is undeniable. This scale gives CBDCs something private crypto never had: institutional legitimacy and massive resource backing.

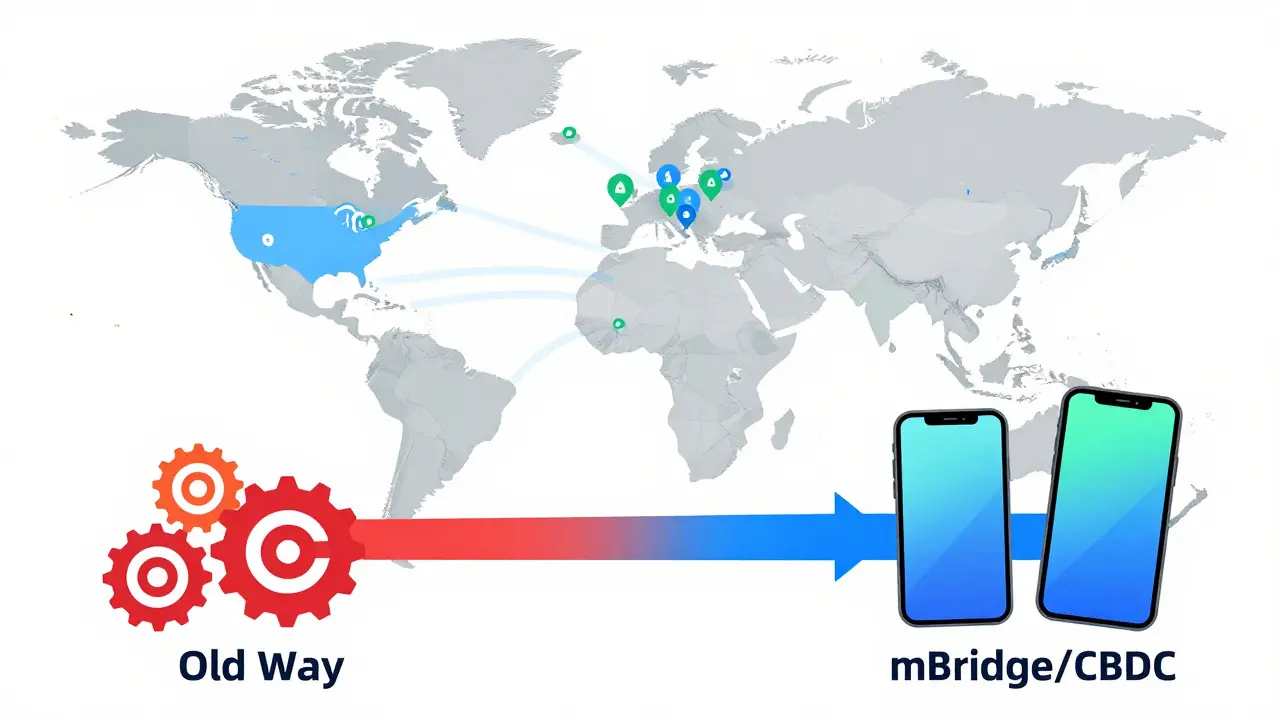

Cross-Border Payments: The Battleground for Utility

If there is one area where CBDCs directly threaten private cryptocurrencies, it is cross-border payments. For years, Bitcoin and stablecoins offered a faster, cheaper alternative to traditional banking wires. Now, governments are building their own high-speed rails.

In 2025, $59 billion worth of cross-border transactions were processed via CBDCs, a 45% increase from the previous year. This growth is driven by major projects like mBridge and Project Dunbar, which involve 29 countries testing interoperability. These initiatives aim to solve the pain points of traditional banking: slow settlement times and high fees.

| Feature | Private Cryptocurrencies (e.g., Bitcoin, Stablecoins) | CBDC Initiatives (e.g., mBridge) |

|---|---|---|

| Regulatory Status | Uncertain, varies by jurisdiction | Legal tender, government-backed |

| Settlement Speed | Minutes to hours (network dependent) | Near-instant (intra-day) |

| Cost | Variable gas fees, can spike | Low, subsidized by central banks |

| Interoperability | Requires bridges/exchanges | Built-in via bilateral agreements |

| Primary Goal | Decentralization, censorship resistance | Efficiency, monetary policy control |

The key difference lies in integration. Twenty-six central banks report that interoperability with private digital payment systems is a major focus. Imagine sending money from your phone wallet directly to someone in another country, settled instantly in local currency, without needing to swap through a volatile asset like Ethereum. That is the promise of CBDCs. While private crypto offers freedom, CBDCs offer frictionless compliance.

Regulation as a Weapon: Compliance vs. Freedom

Here is where the "restrictions" part of the title becomes real. Private cryptocurrencies thrive on ambiguity. They operate in a gray zone that allows for innovation but also attracts scrutiny. CBDCs, by contrast, are born out of regulation.

Forty-eight percent of countries involved in cross-border CBDC projects have aligned their Anti-Money Laundering (AML) and Counter-Financing of Terrorism (CFT) regulations. Thirty-eight percent are even exploring blockchain-based identity verification systems. This means that using a CBDC likely requires you to be who you say you are. There is no anonymity.

For users who value privacy, this is a dealbreaker. Private cryptocurrencies, especially those focused on privacy like Monero or Zcash, offer a layer of separation from state surveillance. CBDCs do not. In fact, some experts worry that CBDCs could allow governments to enforce sanctions more aggressively or even program money to expire, influencing consumer behavior directly.

However, for businesses and institutions, this regulatory clarity is a feature, not a bug. Knowing that your transaction complies with international AML standards reduces risk. As the IMF noted in October 2024, careful design of CBDCs-including access criteria and holding limits-can mitigate adverse effects on monetary operations. This level of control is impossible with decentralized networks.

Security and Stability: Who Holds the Keys?

Cybersecurity is a critical factor in this competition. Over 100 central banks view modernizing payment systems as an opportunity to build resilient infrastructure. The IMF has dedicated research to cyber resilience in CBDC ecosystems, acknowledging that these systems create vast, complex environments that amplify existing risks.

Private cryptocurrencies face different security challenges. Your responsibility is your own. If you lose your seed phrase, your money is gone forever. If a centralized exchange gets hacked, you might lose everything. CBDCs, backed by central banks, offer a safety net similar to deposit insurance in traditional banking. However, this comes with a trade-off: the central bank holds the ultimate power. They can freeze accounts, reverse transactions, or adjust interest rates on holdings.

The Atlantic Council highlights a specific risk: potential bank runs. If citizens panic and rapidly convert commercial bank deposits into CBDCs, it could shock interest rates and weaken lending capabilities. To prevent this, many CBDC designs include quantity limits or tiered remuneration structures. These restrictions ensure stability but limit the utility of CBDCs as a speculative asset compared to Bitcoin.

The Future Landscape: Coexistence or Conflict?

So, what does the future look like? It’s unlikely to be a total takeover. Instead, expect a bifurcated system. CBDCs will dominate areas where trust, speed, and regulatory compliance are paramount: everyday retail payments, cross-border trade, and government disbursements. They will serve the unbanked populations in developing economies, offering financial inclusion through official channels.

Private cryptocurrencies will retreat to niches where their core values shine: censorship resistance, decentralized governance, and speculative investment. Bitcoin may become a "digital gold" store of value, while Ethereum and other smart contract platforms continue to host decentralized applications (dApps) that governments cannot easily shut down.

The competition will drive innovation. CBDCs will force private crypto to improve user experience and security. Private crypto will push central banks to respect privacy concerns and avoid overly restrictive policies. As we move through the remainder of the 2020s, the success of either system will depend on user adoption, technical performance, and the delicate balance between control and freedom.

Will CBDCs replace Bitcoin and other cryptocurrencies?

It is unlikely that CBDCs will completely replace private cryptocurrencies. CBDCs are designed for efficiency, stability, and regulatory compliance, making them ideal for daily transactions and cross-border payments. Private cryptocurrencies like Bitcoin offer decentralization, censorship resistance, and speculative value, which CBDCs explicitly lack. The two systems will likely coexist, serving different user needs and use cases.

How do CBDCs affect privacy compared to private crypto?

CBDCs generally offer less privacy than private cryptocurrencies. Since CBDCs are issued by central banks, they are subject to strict Anti-Money Laundering (AML) and Know Your Customer (KYC) regulations. Transactions are traceable, and identity verification is often required. Private cryptocurrencies, particularly privacy-focused coins, allow for greater anonymity and pseudonymity, though this is increasingly under regulatory pressure globally.

What are the main risks of CBDC adoption for banks?

A primary risk is the potential for bank runs. If citizens perceive CBDCs as safer than commercial bank deposits, they might rapidly convert their savings into CBDCs during times of financial stress. This could drain liquidity from commercial banks, affecting their ability to lend and potentially destabilizing the broader financial system. To mitigate this, many central banks are considering holding limits or non-interest-bearing designs.

Which countries have already launched CBDCs?

As of 2025-2026, several countries have fully launched CBDCs, including the Bahamas (Sand Dollar), Nigeria (eNaira), Jamaica (JAM-DEX), and Zimbabwe (ZiG). Other nations like China (Digital Yuan/e-CNY) and the European Union (Digital Euro) are in advanced pilot or preparation stages, with full rollout expected in the near future.

Can CBDCs work offline?

Yes, offline functionality is a key feature being developed for many CBDCs. For example, the Reserve Bank of India and the Bank of Japan are actively testing offline payment capabilities. This ensures that digital currency can be used even in areas with poor internet connectivity or during network outages, enhancing accessibility and resilience compared to some online-only private crypto solutions.