For years, trying to trade cryptocurrency in Nigeria is a West African nation that has transformed its financial landscape by officially recognizing digital assets as securities under the Investments and Securities Act 2025 felt like playing a dangerous game of cat and mouse. You’d buy Bitcoin on an exchange, try to withdraw funds to your bank account, and suddenly-boom. Your account frozen. No explanation. Just silence from your bank.

If you are reading this in 2026, those days are officially behind us. But here is the catch: the "restrictions" haven’t disappeared; they have just changed shape. They are no longer arbitrary bans by banks acting on old Central Bank directives. Now, the restrictions are clear, written laws enforced by specific agencies. Trying to "avoid" them by going off-grid or using shady peer-to-peer methods is actually the fastest way to get into trouble today.

The smartest way to avoid penalties, frozen assets, and tax audits is not to hide. It is to comply with the new Investments and Securities Act (ISA) 2025 is the landmark legislation signed by President Bola Ahmed Tinubu that legally recognizes cryptocurrencies as financial instruments in Nigeria. This guide breaks down exactly how to operate legally, which platforms to use, and how to handle your taxes so you can trade without looking over your shoulder.

Why the Old Tricks Don't Work Anymore

Remember when you could just use any P2P platform and link it to a random savings account? That era ended when the regulatory framework shifted. In 2017, the Central Bank of Nigeria (CBN) issued circulars restricting banks from facilitating crypto transactions. Then, in 2021, they escalated this by freezing accounts associated with crypto activities. It was chaotic.

But in late 2023, the CBN lifted that ban. More importantly, in March 2025, the ISA 2025 became law. This didn’t just lift restrictions; it created a structured environment where the Securities and Exchange Commission (SEC) is the primary regulatory body responsible for licensing and overseeing virtual asset service providers in Nigeria now holds the keys to the kingdom.

Here is the reality check: If you use an unlicensed exchange or bypass Know Your Customer (KYC) checks, you aren’t avoiding restrictions. You are operating illegally. The SEC, working with the Economic and Financial Crimes Commission (EFCC), now has enhanced powers to access telecommunications records and investigate fraud. Using unregulated channels makes you a target for these investigations, not a free agent.

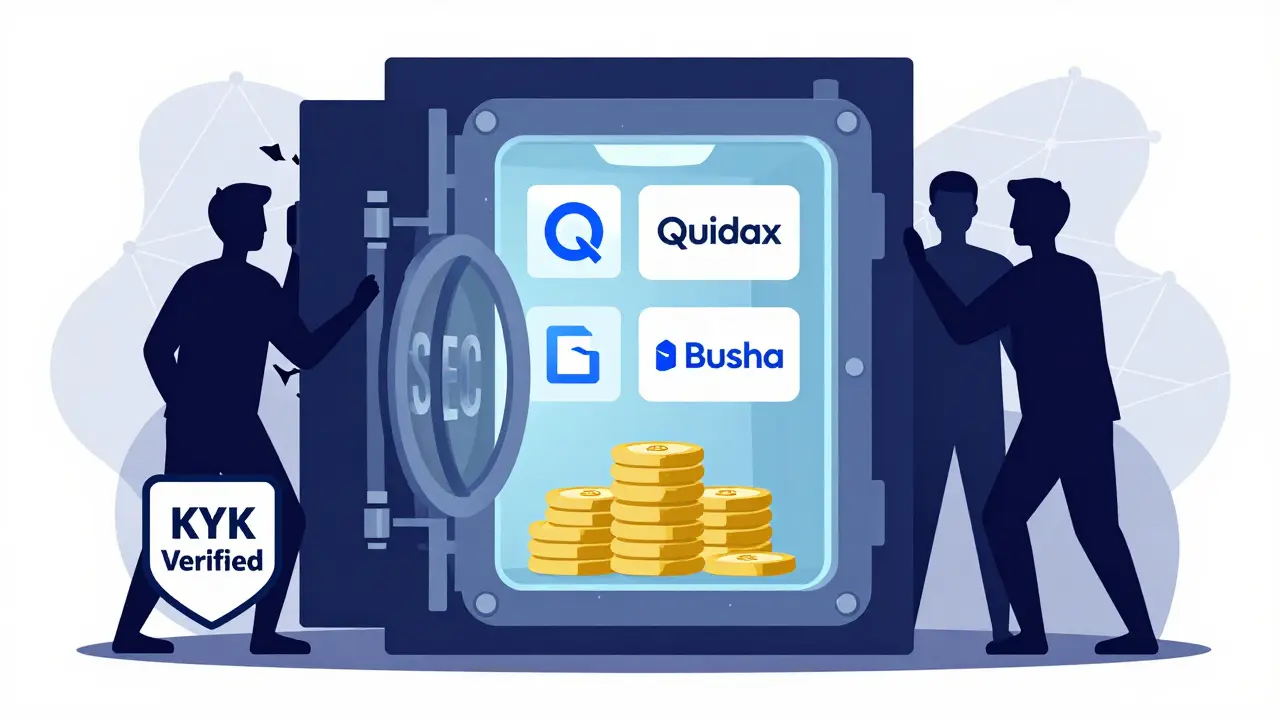

Step 1: Only Use SEC-Licensed Exchanges

The single most important step to staying out of trouble is choosing the right platform. Under the new guidelines, only Virtual Asset Service Providers (VASPs) that are licensed by the SEC can offer services to Nigerian residents with full banking integration.

Why does this matter? Because licensed exchanges are the only ones allowed to open corporate bank accounts. When you trade on a licensed platform, your money moves through compliant channels. Banks recognize these transactions. When you trade on an unlisted app, banks see the deposit as suspicious because there is no regulatory handshake between the exchange and the financial system.

Who is licensed? As of mid-2026, the SEC has approved several major players. Platforms like Quidax is one of the first cryptocurrency exchanges to receive official licensing from the Nigerian SEC, allowing it to operate legally with banking partnerships and Busha is a licensed Nigerian crypto exchange known for robust security features and compliance with SEC regulations have gone through the rigorous vetting process. These platforms offer improved banking integration and customer protection measures.

What to avoid: Do not use offshore exchanges that do not register with the Nigerian SEC. While you might technically be able to create an account, withdrawing fiat currency (Naira) to your local bank will likely trigger alerts. The bank’s compliance team will ask for proof of transaction origin. If your exchange isn’t on the SEC’s whitelist, you cannot provide that proof. Result? Frozen funds.

Step 2: Embrace KYC and AML Procedures

I know what you’re thinking. "I liked crypto because it was private." I get it. But privacy and anonymity are two different things, and the latter is dead in Nigeria’s regulated market. To avoid restrictions, you must fully complete the Know Your Customer (KYC) process.

This means uploading your National ID, providing proof of address, and sometimes even undergoing biometric verification. Licensed exchanges are required to implement strict Anti-Money Laundering (AML) procedures. They report large or suspicious transactions to the Nigerian Financial Intelligence Unit (NFIU).

Pro Tip: Keep your personal information consistent across all platforms. If your name on Binance differs slightly from your name on your bank account due to a typo, it creates a red flag. Ensure every detail matches your government-issued ID perfectly. This reduces the friction when banks verify your source of funds.

Step 3: Understand the New Tax Rules (Effective Jan 1, 2026)

Avoiding restrictions also means paying your fair share. With the Nigerian Tax Administration Act 2025, the government has clarified how crypto is taxed. Ignorance is no longer a valid defense. As of January 1, 2026, crypto assets are treated as property for tax purposes.

Here is how the math works for individuals:

- Taxable Events: You only pay tax when you sell or exchange crypto for profit. Simply holding Bitcoin does not trigger a tax bill.

- Income Tax Rate: Individual profits are subject to personal income tax on a sliding scale, capped at 25%.

- VAT: Companies charge a 7.5% Value Added Tax (VAT) on transaction fees. This is usually deducted automatically at checkout, but you need to be aware of it.

For Businesses: If you run a crypto-related business, the stakes are higher. Corporate income tax is 20% for annual earnings between ₦25 million and ₦100 million, and 30% for earnings exceeding ₦100 million.

How to Stay Compliant: Maintain detailed records of every transaction. Note the date, amount, value in Naira at the time of purchase, and value at the time of sale. Many licensed exchanges now provide annual tax reports. Download these. If you are audited, having a clear paper trail proves you are a legitimate investor, not a money launderer.

Comparison: Licensed vs. Unlicensed Platforms

| Feature | SEC-Licensed Exchange | Unlicensed/Offshore Platform |

|---|---|---|

| Bank Integration | Seamless. Banks recognize deposits/withdrawals. | Risky. High chance of account freezes. |

| Legal Protection | High. Covered by consumer protection laws. | None. No recourse if the platform fails. |

| KYC Requirements | Mandatory and strict. | Often lax or optional (initially). |

| Tax Reporting | Automated assistance available. | You must manually track everything. |

| Regulatory Risk | Low. Operating within the law. | High. Subject to sudden blocks or bans. |

What About NFTs and DeFi?

The ISA 2025 draws a clear line between investment products and art. If you are buying an NFT that promises future returns or dividends, it is considered a security. It falls under SEC oversight. You must buy it through a licensed channel.

However, artistic NFTs-those bought purely for collection or display-are currently unaffected by securities regulations. You can trade these more freely, though standard anti-fraud laws still apply.

Decentralized Finance (DeFi) protocols are a gray area. The current framework focuses on centralized exchanges. While using DeFi isn’t explicitly banned, moving fiat currency (Naira) directly into DeFi wallets is difficult because banks monitor outgoing transfers to unknown addresses. Most savvy users bridge their funds via a licensed exchange first, converting Naira to stablecoins, then moving those stablecoins to a non-custodial wallet for DeFi interactions. Just remember: once your money leaves the licensed ecosystem, you lose the layer of banking protection.

Common Pitfalls to Avoid in 2026

Even with clear laws, mistakes happen. Here are the most common ways Nigerians accidentally break regulations:

- Mixing Personal and Business Funds: If you trade for your employer or manage funds for others, keep those accounts separate. Using a personal wallet for business transactions violates corporate governance standards and complicates tax reporting.

- Ignoring Small Transactions: Some users think small trades don’t count toward taxable income. They do. Aggregated gains over the year are what matter. Track every satoshi.

- Using Multiple Bank Accounts to Hide Activity: Splitting deposits across five different banks to stay under reporting thresholds is a classic money laundering tactic. The NFIU uses algorithms to detect this pattern instantly. It looks worse than being honest about one large transaction.

- Falling for Ponzi Schemes: The ISA 2025 explicitly bans Ponzi schemes. If a platform promises guaranteed daily returns of 1-2%, it is illegal. Report it. Participating in an illegal scheme offers zero legal protection if the rug pull happens.

The Path Forward: Financial Inclusion, Not Exclusion

Nigeria’s shift from restriction to regulation is a win for serious investors. According to CoinGecko data, Nigeria consistently shows the highest crypto interest levels in Africa. The government wants this energy channeled into innovation, job creation, and foreign investment, not underground economies.

By sticking to SEC-licensed platforms like Quidax and Busha, completing your KYC, and keeping accurate tax records, you aren’t just avoiding restrictions. You are securing your assets. You are ensuring that when you make a profit, you can spend it without fear. The wild west is closed. Welcome to the regulated market.

Is it legal to own cryptocurrency in Nigeria in 2026?

Yes, it is fully legal. The Investments and Securities Act (ISA) 2025 officially recognizes digital assets as financial securities. Ownership is protected, provided you engage with licensed Virtual Asset Service Providers (VASPs) and comply with tax obligations.

Which crypto exchanges are licensed by the SEC in Nigeria?

As of mid-2026, prominent licensed exchanges include Quidax and Busha. These platforms have passed the SEC's rigorous vetting process and are permitted to offer banking services to their users. Always check the latest list on the official SEC website before registering, as the approval pipeline is active.

Do I need to pay tax on my crypto profits?

Yes. Under the Nigerian Tax Administration Act 2025, crypto assets are treated as property. You must pay personal income tax on profits realized from sales or exchanges. The rate follows the standard sliding scale, capped at 25% for individuals. Failure to declare these gains can lead to penalties.

Can I still use Peer-to-Peer (P2P) trading?

You can use P2P features offered by licensed exchanges, but you must follow the platform's rules. Direct P2P transfers outside of regulated platforms carry high risks of fraud and account freezing. Banks may flag direct transfers to individuals if they lack proper documentation of the underlying crypto transaction.

What happens if I use an unlicensed exchange?

Using an unlicensed exchange exposes you to significant risk. Your bank account may be frozen because the institution cannot verify the legitimacy of the transaction partner. Additionally, you have no legal recourse if the exchange collapses or engages in fraudulent activity, as it operates outside the protective scope of Nigerian securities law.